First-time homebuyers often turn to FHA loans for their mortgages because they have more flexible approval requirements. For instance, FHA loans only require 3.5% down and a credit score of 620 or lower, compared to the 6% required for a conventional loan. There are also no income verification or home appraisal requirements. The FHA streamline program has another major advantage: you can apply for an FHA loan even though you own another property. Except if you're refinancing the home as an investment, however, you can't refinance it into a mortgage. Moreover, the new mortgage cannot be an adjustable-rate mortgage (ARM) or a cash-out refinance.

Limits to multiple FHA loans

There are limitations on the number of FHA loans that a borrower may have at once. Borrowers are limited to one FHA loan at a given time. The first must be paid off before they can apply for the second. There are exceptions. In certain situations, two FHA loans may be granted to a borrower.

Federal Housing Administration (HUD), determines the maximum amount you can borrow for an FHA loan. The number of units you have and the location of your property will affect the amount of money that you can borrow. A home with multiple units will have its limits increase.

Minimum down payment

To qualify for an FHA loan, you need to put down at least 10 percent of the purchase price. You can also get assistance from the state and government for your down payment if money is tight. As part of your downpayment, you can also get a gift from family or friends. Make sure the gift is a gift, not a loan, as the FHA cannot approve a loan that involves borrowing to pay for the down payment.

In addition to the down payment, you must meet credit and income requirements. You must also provide proof of your identity and asset accounts to qualify for an FHA loan. A minimum 500 credit score is required to qualify for an FHA loan. Low credit scores can lead to higher interest rates, so make sure you pay close attention to your score.

For an FHA loan you will need to meet the following requirements

An FHA loan application requires you to show proof that you can afford your monthly payments. You can prove income by providing proof, such as pay statements, bank statements or W-2 income statements. Also, you should have enough financial reserves to pay the down payment and closing costs for a new house.

Also, consider the minimum debt to income ratio (DTI), when applying for a loan. The FHA requires borrowers to maintain a DTI of under 43%. Some lenders will accept applicants with higher DTIs. Your credit score is also important in determining whether you are eligible for a loan.

You must meet all requirements in order to be eligible for an FHA Loan after a waiting time

FHA loans are not easy to get a mortgage for people who have low credit ratings or don't have enough money down. Since this type of loan is insured by the government, it usually has lower interest rates than conventional mortgages. FHA lenders don't charge risk-based mortgage insurance. This means that even borrowers who have poor credit ratings will be approved with a higher chance.

There are some questions you might have about your eligibility for a new loan if your home has been foreclosed. For an FHA mortgage you must meet some criteria. A reduced income of at least 20%, positive credit reports, and a downpayment of at least 20% are the main requirements. Be aware of the FHA loan eligibility rules, which will make it easier for your to get approved.

There are several ways you can qualify for an FHA Loan after the waiting period

After completing the waiting period, there are many ways you can qualify for an FHA loan. One way is to show lenders that you have recovered your credit and made twelve months of mortgage payments before your waiting period began. For an FHA loan you need a credit score of at least 580. Some lenders require a higher score if you have recently been through a foreclosure or other event that negatively affected your credit.

Lenders will sometimes make exceptions for borrowers who have filed bankruptcy. One reason for filing bankruptcy is financial hardship. Because bankruptcy is a derogatory mark on your credit score, many people who file bankruptcy end up selling their homes. You can still qualify for an FHA loan if you prove your financial recovery after bankruptcy.

FAQ

What should I do before I purchase a house in my area?

It all depends on how long your plan to stay there. It is important to start saving as soon as you can if you intend to stay there for more than five years. You don't have too much to worry about if you plan on moving in the next two years.

Are flood insurance necessary?

Flood Insurance covers flood damage. Flood insurance protects your belongings and helps you to pay your mortgage. Learn more information about flood insurance.

What are the disadvantages of a fixed-rate mortgage?

Fixed-rate mortgages have lower initial costs than adjustable rates. Also, if you decide to sell your home before the end of the term, you may face a steep loss due to the difference between the sale price and the outstanding balance.

What is a "reverse mortgage"?

A reverse mortgage allows you to borrow money from your house without having to sell any of the equity. This reverse mortgage allows you to take out funds from your home's equity and still live there. There are two types: government-insured and conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers repayments.

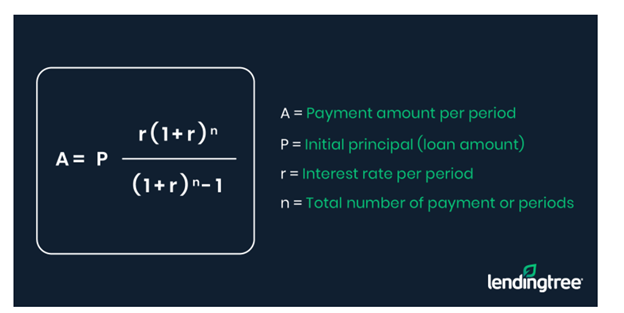

How do I calculate my rate of interest?

Interest rates change daily based on market conditions. The average interest rate during the last week was 4.39%. The interest rate is calculated by multiplying the amount of time you are financing with the interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to Manage a Property Rental

Although renting your home is a great way of making extra money, there are many things you should consider before you make a decision. We will show you how to manage a rental home, and what you should consider before you rent it.

This is the place to start if you are thinking about renting out your home.

-

What should I consider first? Take a look at your financial situation before you decide whether you want to rent your house. If you have any debts such as credit card or mortgage bills, you might not be able pay for someone to live in the home while you are away. It is also important to review your budget. If you don't have enough money for your monthly expenses (rental, utilities, and insurance), it may be worth looking into your options. It may not be worth it.

-

How much does it cost to rent my home? There are many factors that go into the calculation of how much you can charge to let your home. These factors include your location, the size of your home, its condition, and the season. Prices vary depending on where you live so it's important that you don't expect the same rates everywhere. Rightmove estimates that the market average for renting a 1-bedroom flat in London costs around PS1,400 per monthly. This means that if you rent out your entire home, you'd earn around PS2,800 a year. It's not bad but if your property is only let out part-time, it could be significantly lower.

-

Is it worth it? There are always risks when you do something new. However, it can bring in additional income. Make sure that you fully understand the terms of any contract before you sign it. Your home will be your own private sanctuary. However, renting your home means you won't have to spend as much time with your family. Make sure you've thought through these issues carefully before signing up!

-

Are there any benefits? There are benefits to renting your home. There are plenty of reasons to rent out your home: you could use the money to pay off debt, invest in a holiday, save for a rainy day, or simply enjoy having a break from your everyday life. It's more fun than working every day, regardless of what you choose. Renting could be a full-time career if you plan properly.

-

How do you find tenants? Once you've decided that you want to rent out, you'll need to advertise your property properly. You can start by listing your property online on websites such as Rightmove and Zoopla. Once potential tenants contact you, you'll need to arrange an interview. This will help you evaluate their suitability as well as ensure that they are financially secure enough to live in your home.

-

How do I ensure I am covered? If you fear that your home will be left empty, you need to ensure your home is protected against theft, damage, or fire. You will need to insure the home through your landlord, or directly with an insurer. Your landlord will typically require you to add them in as additional insured. This covers damages to your property that occur while you aren't there. If you are not registered with UK insurers or if your landlord lives abroad, however, this does not apply. In such cases, you will need to register for an international insurance company.

-

Even if your job is outside the home, you might feel you cannot afford to spend too much time looking for tenants. It's important to advertise your property with the best possible attitude. You should create a professional-looking website and post ads online, including in local newspapers and magazines. It is also necessary to create a complete application form and give references. While some people prefer to handle everything themselves, others hire agents who can take care of most of the legwork. It doesn't matter what you do, you will need to be ready for questions during interviews.

-

What should I do once I've found my tenant? If you have a contract in place, you must inform your tenant of any changes. You can negotiate details such as the deposit and length of stay. While you might get paid when the tenancy is over, utilities are still a cost that must be paid.

-

How do you collect the rent? When the time comes for you to collect the rent you need to make sure that your tenant has been paying their rent. If they haven't, remind them. After sending them a final statement, you can deduct any outstanding rent payments. If you're having difficulty getting hold of your tenant you can always call police. They will not usually evict someone unless they have a breached the contract. But, they can issue a warrant if necessary.

-

What can I do to avoid problems? You can rent your home out for a good income, but you need to ensure that you are safe. Make sure you have carbon monoxide detectors installed and security cameras installed. Make sure your neighbors have given you permission to leave your property unlocked overnight and that you have enough insurance. You should not allow strangers to enter your home, even if they claim they are moving in next door.