A home refinance calculator is an automated tool that enables homeowners to estimate the monetary effects of varying variables. It is simple to use and can help homeowners save time and money. A home refinance calculator is a tool that homeowners can use to make informed financial decisions. A home refinance tool can help you determine the best rate to fit your needs and your budget by simply entering some basic data.

Tax-free cash-out refinance

A cash-out home refinance can be a great way for home improvements to be made without paying taxes. A cash-out refinance will not be free of cost. It is debt. You will need to make interest payments. You won't be required to report the income as income under the Tax Cuts and Jobs Act of 2018.

Refinances of homes with cash are exempt from taxes because the money is not treated as income. The IRS considers the equity that you receive from a cash-out refinance as an additional loan, rather than cash income. It's important that you understand that cash out home refinances are different than traditional mortgages. There are also guidelines that govern the amount of your mortgage points that can be deducted.

Refinance to a more long-term loan term

Refinancing is a great option to reduce your monthly payments as well as take advantage lower interest rates. Refinancing your home may help you pay off your mortgage quicker and build equity earlier. But there are also risks and disadvantages to refinancing your home. You can use our mortgage calculator to calculate your monthly costs.

Consider the loan term length when refinancing your house. A shorter term can help you save thousands in interest over its life.

Refinance has tax benefits

There might be tax benefits to refinancing your house. While refinancing costs can't be tax deductible, your lender's appraisal might. This could be due escalating property costs or the fact that the appraisal of your lender was higher than what the tax authority assessed.

Refinancing comes with its fair share of tax benefits. One of those benefits is the possibility to deduct points from your mortgage. Over the term of your loan, points, which equal 1% of the loan amount, can be deducted. This deduction is available if you refinance your primary property or another qualifying property. If you refinance to receive a lower rate of interest, you can also subtract your discount points.

Common fees associated with refinancing

It is important to understand the costs associated with home refinance loans. There are many lenders that charge an application fee. This can range from $75 to $300. This fee covers administrative costs such as evaluating loan eligibility and assessing loan eligibility. Lenders may also charge a loan origination cost of 0.5% to 1.5% depending on the amount of the loan. Additionally, your lender may charge you for a title search, which can cost between $200 and $400.

A loan with higher interest rates is generally more expensive than one that has a lower rate. The loan balance can be used to finance fees if you have sufficient equity in your home. Alternately, you may cash out some money you saved. Refinances should be discussed with your lender to determine if there are any savings.

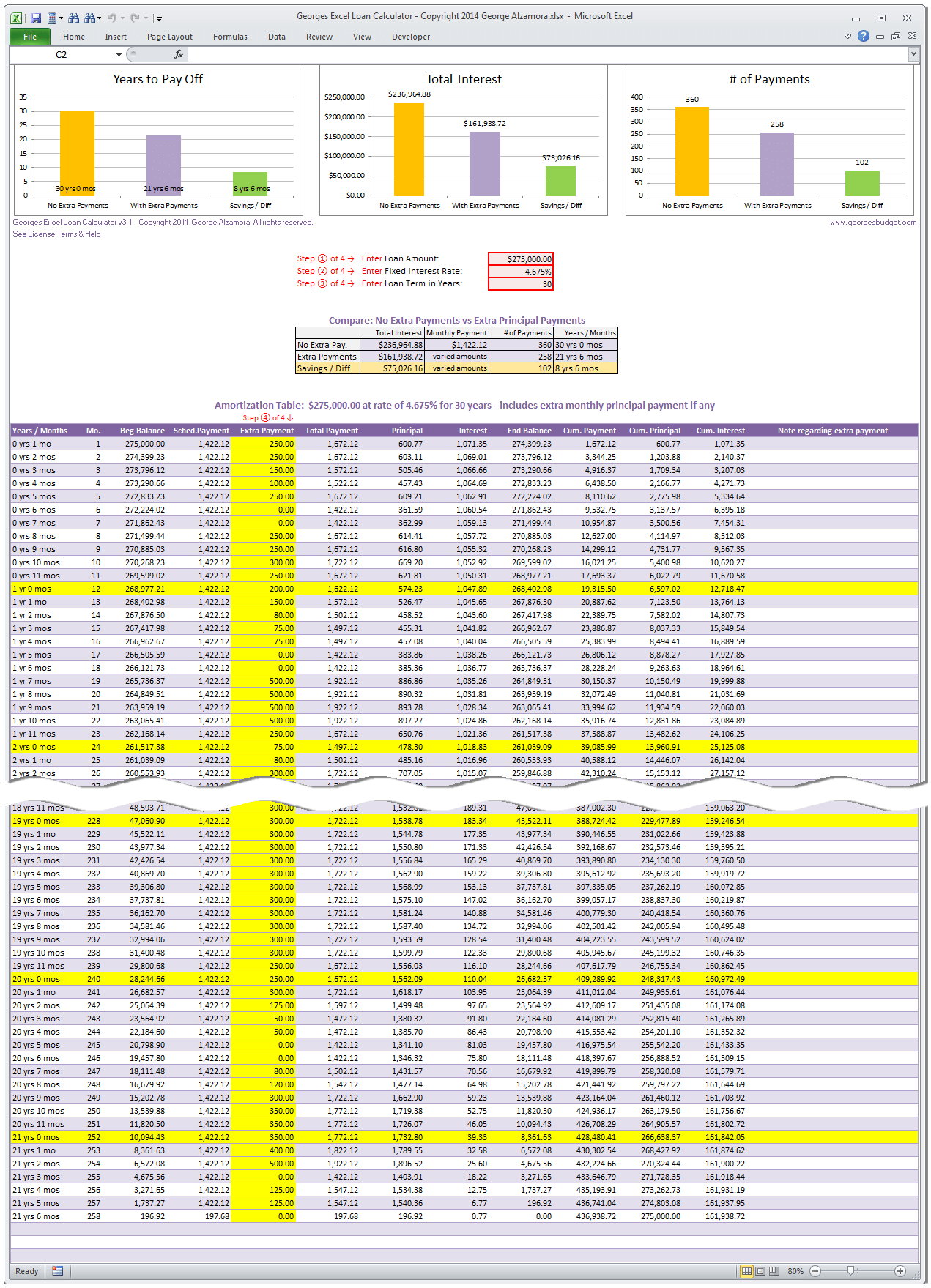

Calculator

A home finance calculator will help you figure out how much you can pay for your home. This calculator can be used to calculate your monthly payments as well as the down payment amount. The calculator will calculate your monthly property taxes and homeowners' insurance. Many times, the calculator will calculate these costs for you automatically, making it as easy as possible.

You can also use the calculator to calculate your monthly payments based on your downpayment, interest rate, home value, and other factors. You can either enter a certain amount or a range of money. For example, if you're planning to purchase a $150,000 home, the calculator will calculate the total monthly payment you'll need to pay. Once you know what your monthly payment will be, you can start comparing different mortgage rates.

FAQ

Can I buy a house in my own money?

Yes! Yes. There are programs that will allow those with small cash reserves to purchase a home. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. Visit our website for more information.

Do I need flood insurance?

Flood Insurance protects you from flooding damage. Flood insurance helps protect your belongings, and your mortgage payments. Learn more about flood coverage here.

How can you tell if your house is worth selling?

If you have an asking price that's too low, it could be because your home isn't priced correctly. If you have an asking price well below market value, then there may not be enough interest in your home. To learn more about current market conditions, you can download our free Home Value Report.

How can I calculate my interest rate

Market conditions impact the rates of interest. The average interest rate over the past week was 4.39%. Multiply the length of the loan by the interest rate to calculate the interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

External Links

How To

How to Rent a House

People who are looking to move to new areas will find it difficult to find houses to rent. But finding the right house can take some time. There are many factors that can influence your decision-making process in choosing a home. These factors include size, amenities, price range, location and many others.

We recommend you begin looking for properties as soon as possible to ensure you get the best deal. Also, ask your friends, family, landlords, real-estate agents, and property mangers for recommendations. This will give you a lot of options.