You might consider applying for a conventional loan, if you have a high DTI or are concerned about an excessive interest rate. This type of loan can be obtained with as little 3% down and is very convenient. This type of loan comes with its risks. You need to take certain steps to reduce your DTI before applying for a conventional loan.

Preparing to apply for a conventional mortgage

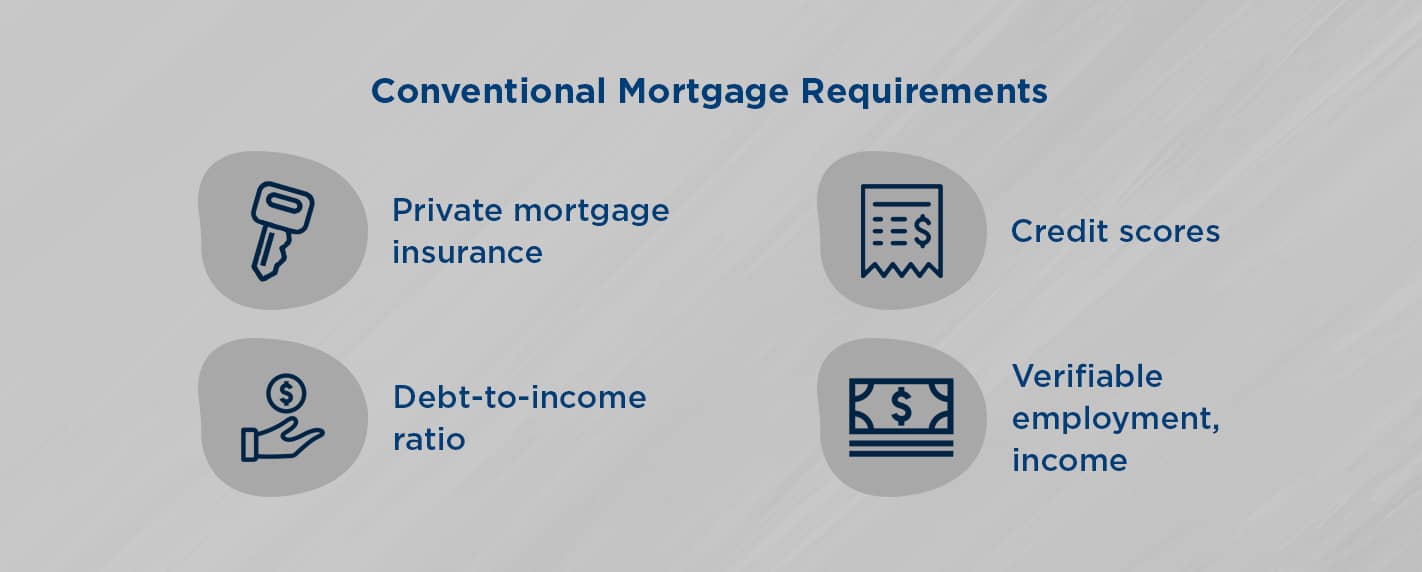

A conventional loan is a good option if your company needs financing. These loans are typically quick and easy to obtain, but they also require a high credit score and other financial qualifications. People with less than perfect credit have other options. Low interest rates, low fees and flexible payback options can all be found.

First, make sure you have a clear picture of your financial situation before applying for a conventional loan. You should pay off all debts, increase your income and save money for a downpayment. You can improve your chances of approval by following these guidelines and receive the funding that you need.

Get a conventional loan as low as 3.3% down

For many home buyers, a conventional loan that requires as little as 3 percent down is an excellent option. If you have good credit, this type of loan is likely to be the most affordable. The down payment is small, so you can still save money for other purchases related to your home.

There are two types of these loans. First, there is the Fannie Mae 3% down loan. This is for first-time homebuyers. To be eligible for this loan, you must have not owned a home for less than three years. A federally insured loan with 3% down payment is also an option.

Convenience of a Conventional Loan

A conventional mortgage is the most common type of mortgage. It can be used for many reasons. They are easier and more flexible than other types of mortgages. A conventional loan doesn't need mortgage insurance and has an extremely low interest rate.

While a conventional loan cannot be backed by federal government, it is still popular for those with good credit, steady income and sufficient down payment funds. This loan is also an option for first-time homebuyers and those with less than perfect credit.

There are risk of default on a conventional loan

Conventional loans are more affordable than government-backed mortgages. However, they also come with their own set risks. These loans are not insured by the federal government and lenders can lose a lot if you default. These loans are more difficult to get than those that are backed by the government.

Conventional loans fall into two categories: conforming and non-conforming. Conforming loans are those that conform to lending standards set by Fannie Mae & Freddie Mac. Non-conforming loans exceed conforming loan limits. Non-conforming loans will typically have higher interest and underwriting requirements as well as higher down payments.

FAQ

Should I use an mortgage broker?

A mortgage broker is a good choice if you're looking for a low rate. A broker works with multiple lenders to negotiate your behalf. However, some brokers take a commission from the lenders. You should check out all the fees associated with a particular broker before signing up.

What is reverse mortgage?

A reverse mortgage is a way to borrow money from your home without having to put any equity into the property. It allows you to borrow money from your home while still living in it. There are two types of reverse mortgages: the government-insured FHA and the conventional. If you take out a conventional reverse mortgage, the principal amount borrowed must be repaid along with an origination cost. FHA insurance covers the repayment.

What are the advantages of a fixed rate mortgage?

A fixed-rate mortgage locks in your interest rate for the term of the loan. This guarantees that your interest rate will not rise. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

Do I require flood insurance?

Flood Insurance covers flood damage. Flood insurance protects your possessions and your mortgage payments. Learn more about flood insurance here.

How long does it take for my house to be sold?

It all depends upon many factors. These include the condition of the home, whether there are any similar homes on the market, the general demand for homes in the area, and the conditions of the local housing markets. It may take up to 7 days, 90 days or more depending upon these factors.

How can I determine if my home is worth it?

You may have an asking price too low because your home was not priced correctly. A home that is priced well below its market value may not attract enough buyers. Our free Home Value Report will provide you with information about current market conditions.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to buy a mobile house

Mobile homes can be described as houses on wheels that are towed behind one or several vehicles. Mobile homes have been around since World War II when soldiers who lost their homes in wartime used them. People today also choose to live outside the city with mobile homes. These homes are available in many sizes and styles. Some houses are small, others can accommodate multiple families. Even some are small enough to be used for pets!

There are two main types for mobile homes. The first type of mobile home is manufactured in factories. Workers then assemble it piece by piece. This occurs before delivery to customers. A second option is to build your own mobile house. You'll need to decide what size you want and whether it should include electricity, plumbing, or a kitchen stove. Next, ensure you have all necessary materials to build the house. You will need permits to build your home.

Three things are important to remember when purchasing a mobile house. You may prefer a larger floor space as you won't always have access garage. A model with more living space might be a better choice if you intend to move into your new home right away. You should also inspect the trailer. It could lead to problems in the future if any of the frames is damaged.

Before you decide to buy a mobile-home, it is important that you know what your budget is. It is important that you compare the prices between different manufacturers and models. It is important to inspect the condition of trailers. Although many dealerships offer financing options, interest rates will vary depending on the lender.

Instead of purchasing a mobile home, you can rent one. Renting allows you the opportunity to test drive a model before making a purchase. Renting isn't cheap. Renters usually pay about $300 per month.