The amount that the lender will give you for your mortgage to purchase your home will be reduced if you make a downpayment. A 20% downpayment will, for example. This will reduce the amount of money that the lender will need to return if you stop making payments. It is important that you note that the lender cannot set the down payment requirement. It can also be set by the investor funding the loan.

Savings for down payment

It is important to save for a downpayment on a mortgage in order to purchase a home. This process is similar to running a marathon: it is important to build up your savings one dollar at a time, while making certain that your finances are in order. You can do this by creating a budget, and directing funds to saving for a downpayment.

Re-selling items from your home is a great way to save money on a down payment. This can be done online, at local pawn shops or consignment stores. To raise funds for your down payment, you might also consider selling items at a yard sale. Make sure you include the income of your partner.

Documentation required

You must have the proper documentation to get a mortgage. The lender will need proof of the source of your downpayment funds. Even if it's a check made from any place, it's important to show proof that the funds have come from. Lenders require a downpayment in order to close a loan. There are exceptions.

Most mortgage lenders will request your last two tax returns. Typically, they will require the most recent federal tax returns and state tax returns. Additional income documentation may be required.

Average down payment

This year has seen historic mortgage rates fall to record lows. This is fueling a vibrant housing market. What is the average down payment? It all depends on where you live. The average down payment on a California mortgage was more than $100k in June 2021. In a few other states, it was less than $10k. Your equity will increase the larger your down payments, the lower your mortgage loan, and the smaller your down payment will be.

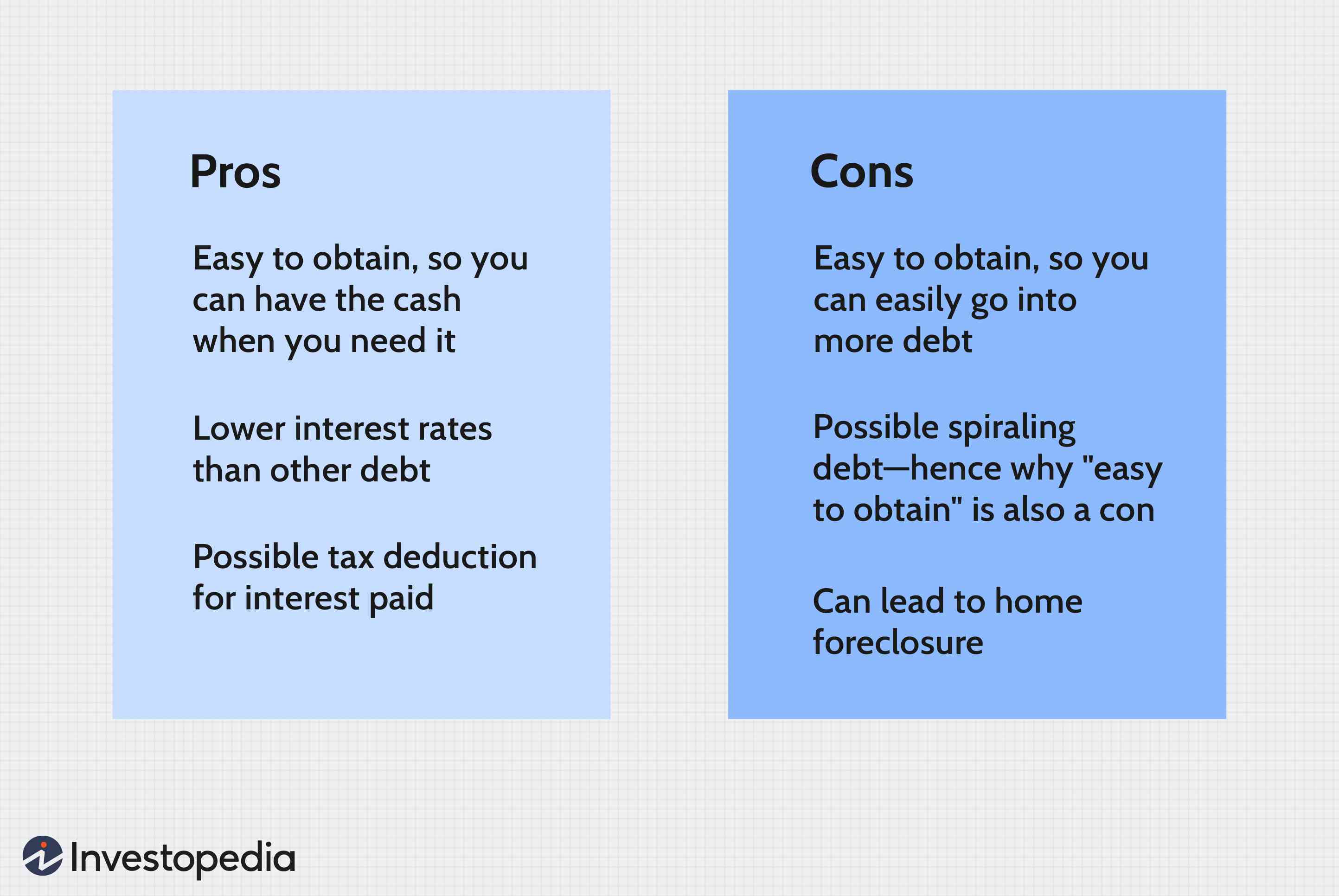

While some lenders require a 20 percent down payment, many people choose to put down a lower amount. A lower down payment will allow you to reach your goal faster. Before choosing a down payment amount, consider the pros and cons of each option.

Savings on PMI

PMI is a way to save money on your mortgage but it comes with a cost. PMI can cost anywhere from 0.3 percent to 1.5 percent of the loan amount. These fees can be added to your monthly payments or paid at closing. This fee can vary between mortgages.

Paying upfront for PMI can help you save money. Although this will reduce your monthly payment it can also result in a higher annual expense which may not be refundable should you move. Another option is to make partial payments each month and save on monthly premiums. This can be particularly useful if you need to save cash early in the year or you don't have a large down payment to put down on a home.

Impact of a down payment on the loan-to-value ratio

Down payments for mortgages have a huge impact on the loan-to-value ratio (LTV). A higher downpayment will result in a lower LTV. Because the LTV ratio is lower, you have more equity in your home. If you have a smaller down payment, you may be able to increase it to reduce your mortgage.

A loan with 80% LTV is available if your down payment exceeds 10% of the total cost. This will lower your chances of default and your monthly payments. Bankrate has a mortgage calculator you can use to calculate how much you will have to deposit on your mortgage.

FAQ

How much money will I get for my home?

The number of days your home has been on market and its condition can have an impact on how much it sells. The average selling price for a home in the US is $203,000, according to Zillow.com. This

Can I buy a house without having a down payment?

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include government-backed loans (FHA), VA loans, USDA loans, and conventional mortgages. More information is available on our website.

Should I rent or own a condo?

Renting might be an option if your condo is only for a brief period. Renting can help you avoid monthly maintenance fees. However, purchasing a condo grants you ownership rights to the unit. You have the freedom to use the space however you like.

How do I fix my roof

Roofs can leak because of wear and tear, poor maintenance, or weather problems. Roofing contractors can help with minor repairs and replacements. For more information, please contact us.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

Finding an apartment is the first step when moving into a new city. This involves planning and research. It includes finding the right neighborhood, researching neighborhoods, reading reviews, and making phone calls. You have many options. Some are more difficult than others. The following steps should be considered before renting an apartment.

-

Researching neighborhoods involves gathering data online and offline. Online resources include Yelp and Zillow as well as Trulia and Realtor.com. Local newspapers, real estate agents and landlords are all offline sources.

-

Find out what other people think about the area. Yelp. TripAdvisor. Amazon.com have detailed reviews about houses and apartments. You can also check out the local library and read articles in local newspapers.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them about what they liked or didn't like about the area. Also, ask if anyone has any recommendations for good places to live.

-

Consider the rent prices in the areas you're interested in. If you think you'll spend most of your money on food, consider renting somewhere cheaper. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Find out more information about the apartment building you want to live in. How big is the apartment complex? What is the cost of it? Is it pet friendly What amenities are there? Are you able to park in the vicinity? Are there any special rules that apply to tenants?