Margin is what determines mortgage rates for 5/1ARMs. It is the difference in the index rate and the interest rate that you pay. While the index rate is subject to change over time, it is generally set at the beginning and remains constant throughout the loan term. The loan's life expectancy will be shorter if the margin is lower.

15-year fixed vs. 5/1ARM

It is important to know the difference between ARM rates (ARM) and fixed rates (15-year), if you are looking for a home mortgage. Although the mortgage types are similar, there are important differences. A 15-year fixed-rate mortgage will have a fixed payment for its entire term. An ARM will adjust its rate of interest based on the mortgage documentation. This means that the monthly payment will be adjusted whenever the index value changes. Fixed-rate mortgages can be more expensive over time because ARMs are shorter in term.

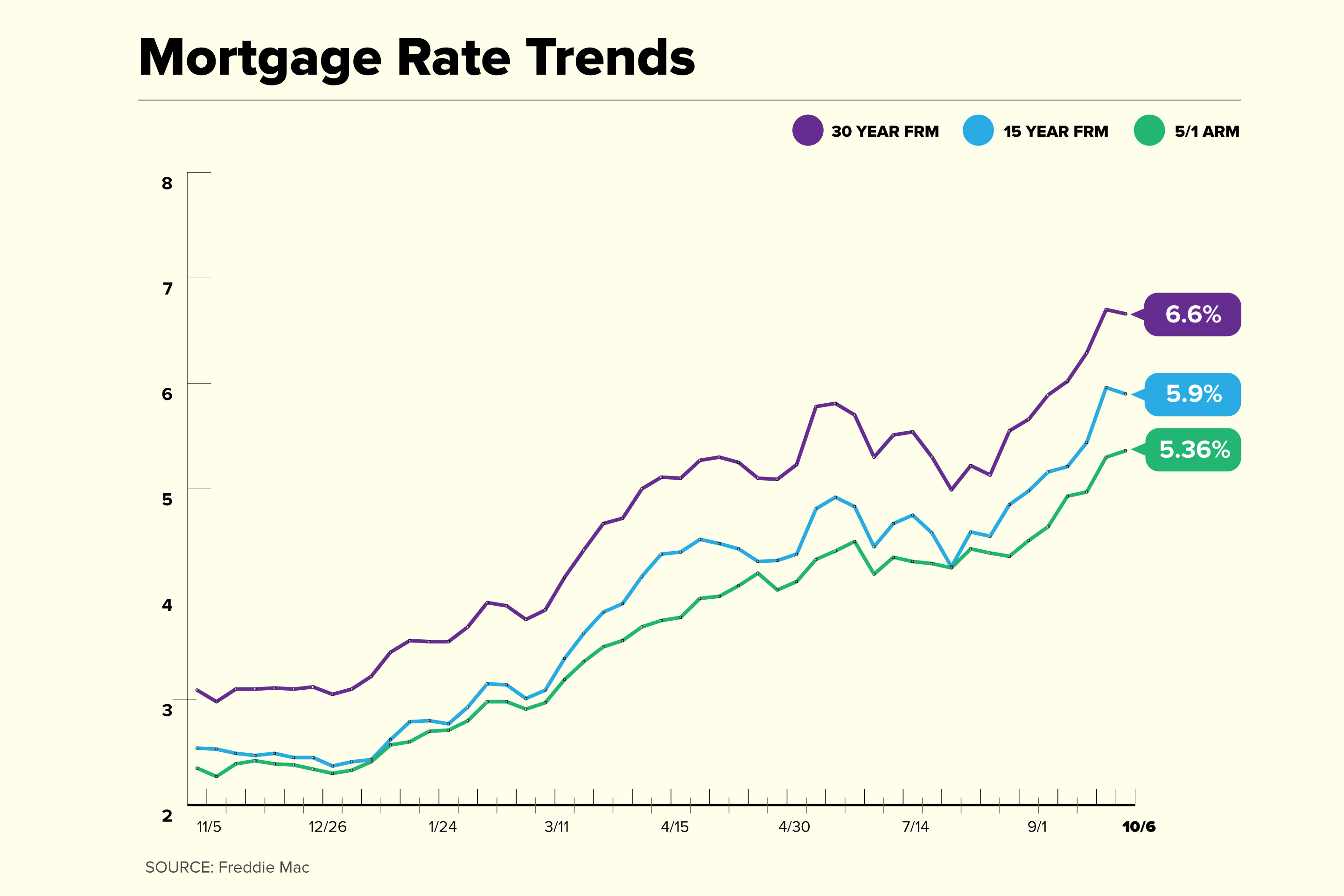

Five-year adjustable rate mortgage rates are more expensive than 15-year fixed rate mortgages. This is due in large part to the lower interest rate on five-year ARMs since the mid-1900s. In 2006, the average 5/1ARM rate was 6.08%. In 2010, that rate fell to 3.82%. The 15-year fixed-rate mortgage is now at 5.90% with a 0.1-point down payment. The 5/1 ARM is at 5.36%, with a deposit of 0.3 points.

Interest rate caps for 5/1 ARMs

The interest rate caps on 5/1 ARMs limit how much the interest rate can increase over the term of the loan. The index, the interest rate for the first year and the margin are all affected by the caps. In some cases, the caps are set to increase once a year or once every two years. In other cases, they are set to increase every five years.

In some instances, the cap may not apply on the initial interest rate. The introductory interest rates are lower than those that would be applicable if the loan were a fixed rate mortgage. The introductory interest rate is often a full percentage point lower than the rate that will be in effect at the end the fixed-rate period of five years. The initial interest rate may rise to a higher rate after the fixed rate period. To prevent this from happening, most ARMs come with an interest rate cap. This can be either a daily or lifetime cap which limits the rate of interest increase over the loan's term.

Interest rate caps on 5/1 ARMs are a key factor in keeping the monthly payments affordable. The higher the interest rate, the higher the monthly payment. It is therefore crucial to check that the interest rates caps are appropriate for your particular situation.

Cost of 5/1 ARM loan

Consider all the potential ramifications of a 5/1ARM loan. This type of loan requires you to pay an interest rate that adjusts based on the market index. These mortgages have caps that limit interest rate increases. The first cap restricts the rate increase that the loan can make during the first one year. The periodic cap caps how much the rate may rise each time the loan is modified.

A 5/1ARM loan typically has a low interest rate which makes it a great option for short-term home ownership. The rate is fixed for five years and then adjusts according to the current interest rate plus a margin. The financial sector is currently eliminating this type of mortgage. The process started in the last year, and will continue until lenders stop offering this type of loan. Changes in financial indicators are some of the reasons for the phase out.

FAQ

How can I repair my roof?

Roofs can leak due to age, wear, improper maintenance, or weather issues. Minor repairs and replacements can be done by roofing contractors. For more information, please contact us.

How much should I save before I buy a home?

It all depends on how long your plan to stay there. Save now if the goal is to stay for at most five years. You don't have too much to worry about if you plan on moving in the next two years.

How can you tell if your house is worth selling?

You may have an asking price too low because your home was not priced correctly. If you have an asking price well below market value, then there may not be enough interest in your home. You can use our free Home Value Report to learn more about the current market conditions.

What are the benefits associated with a fixed mortgage rate?

Fixed-rate mortgages guarantee that the interest rate will remain the same for the duration of the loan. This will ensure that there are no rising interest rates. Fixed-rate loans come with lower payments as they are locked in for a specified term.

What is reverse mortgage?

Reverse mortgages are a way to borrow funds from your home, without having any equity. It allows you to borrow money from your home while still living in it. There are two types available: FHA (government-insured) and conventional. Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers repayments.

Do I need a mortgage broker?

If you are looking for a competitive rate, consider using a mortgage broker. Brokers work with multiple lenders and negotiate deals on your behalf. Some brokers earn a commission from the lender. Before you sign up for a broker, make sure to check all fees.

Are flood insurance necessary?

Flood Insurance protects against damage caused by flooding. Flood insurance helps protect your belongings and your mortgage payments. Learn more information about flood insurance.

Statistics

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to Manage A Rental Property

It can be a great way for you to make extra income, but there are many things to consider before you rent your house. These tips will help you manage your rental property and show you the things to consider before renting your home.

If you're considering renting out your home, here's everything you need to know to start.

-

What is the first thing I should do? Take a look at your financial situation before you decide whether you want to rent your house. You may not be financially able to rent out your house to someone else if you have credit card debts or mortgage payments. Your budget should be reviewed - you may not have enough money to cover your monthly expenses like rent, utilities, insurance, and so on. You might find it not worth it.

-

How much will it cost to rent my house? There are many factors that go into the calculation of how much you can charge to let your home. These factors include your location, the size of your home, its condition, and the season. You should remember that prices are subject to change depending on where they live. Therefore, you won't get the same rate for every place. Rightmove shows that the median market price for renting one-bedroom flats in London is approximately PS1,400 per months. This would translate into a total of PS2,800 per calendar year if you rented your entire home. That's not bad, but if you only wanted to let part of your home, you could probably earn significantly less.

-

Is it worthwhile? Doing something new always comes with risks, but if it brings in extra income, why wouldn't you try it? You need to be clear about what you're signing before you do anything. It's not enough to be able to spend more time with your loved ones. You'll need to manage maintenance costs, repair and clean up the house. Before you sign up, make sure to thoroughly consider all of these points.

-

Is there any benefit? There are benefits to renting your home. There are plenty of reasons to rent out your home: you could use the money to pay off debt, invest in a holiday, save for a rainy day, or simply enjoy having a break from your everyday life. Whatever you choose, it's likely to be better than working every day. Renting could be a full-time career if you plan properly.

-

How do you find tenants? Once you decide that you want to rent out your property, it is important to properly market it. You can start by listing your property online on websites such as Rightmove and Zoopla. You will need to interview potential tenants once they contact you. This will help to assess their suitability for your home and confirm that they are financially stable.

-

How can I make sure I'm covered? You should make sure your home is fully insured against theft, fire, and damage. You will need insurance for your home. This can be done through your landlord directly or with an agent. Your landlord may require that you add them to your additional insured. This will cover any damage to your home while you are not there. This doesn't apply to if you live abroad or if the landlord isn’t registered with UK insurances. You will need to register with an International Insurer in this instance.

-

It's easy to feel that you don't have the time or money to look for tenants. This is especially true if you work from home. However, it is important that you advertise your property in the best way possible. It is important to create a professional website and place ads online. A complete application form will be required and references must be provided. Some prefer to do it all themselves. Others hire agents to help with the paperwork. Either way, you'll need to be prepared to answer questions during interviews.

-

What should I do once I've found my tenant? If you have a current lease in place you'll need inform your tenant about changes, such moving dates. You can negotiate details such as the deposit and length of stay. While you might get paid when the tenancy is over, utilities are still a cost that must be paid.

-

How do you collect the rent? When it comes to collecting the rent, you will need to confirm that the tenant has made their payments. If not, you'll need to remind them of their obligations. After sending them a final statement, you can deduct any outstanding rent payments. If you are having difficulty finding your tenant, you can always contact the police. They will not normally expel someone unless there has been a breach of contract. However, they can issue warrants if necessary.

-

How do I avoid problems? Renting out your house can make you a lot of money, but it's also important to stay safe. Ensure you install smoke alarms and carbon monoxide detectors and consider installing security cameras. It is important to check that your neighbors allow you leave your property unlocked at nights and that you have sufficient insurance. You must also make sure that strangers are not allowed to enter your house, even when they claim they're moving in the next door.