A mortgage is a loan that a financial institution gives to a person or business. The lender expects that the borrower pays the money back, along with interest. A letter of credit is a document that allows a person to borrow from the bank up to a set amount. A lien can be placed on the property's title, making it more difficult to get rid of. A life cap can be added to an adjustable rate mortgage. This means that the interest rate can only be increased for a specific period.

Amortization period

A mortgage refers to a loan that must paid back within a given time. The amortization period is the term used to describe this period. The amortization period can be represented as a table which shows the principal and interest percentages that are paid each month. The amortization schedule also shows the total loan balance. The amortization schedule shows the total loan balance. Typically, early payments are principal and interest.

A mortgage contract's amortization period is one of its most important elements. First-time home buyers may prefer a longer amortization period as it will enable them to pay down their loans more quickly. If you prefer a shorter amortization period you might consider purchasing a home with a lower price.

Interest rate

The interest rate for a mortgage is what the lender charges you to borrow a loan. The annual interest rate is a percentage calculated from the principle amount. This rate will vary depending on the terms of the loan. It will be lower for low-risk borrowers and higher for high-risk borrowers. A term that some borrowers may encounter is the annual percent yield, also known as APY. This is the interest charged by a bank to borrowers on top o the principal amount.

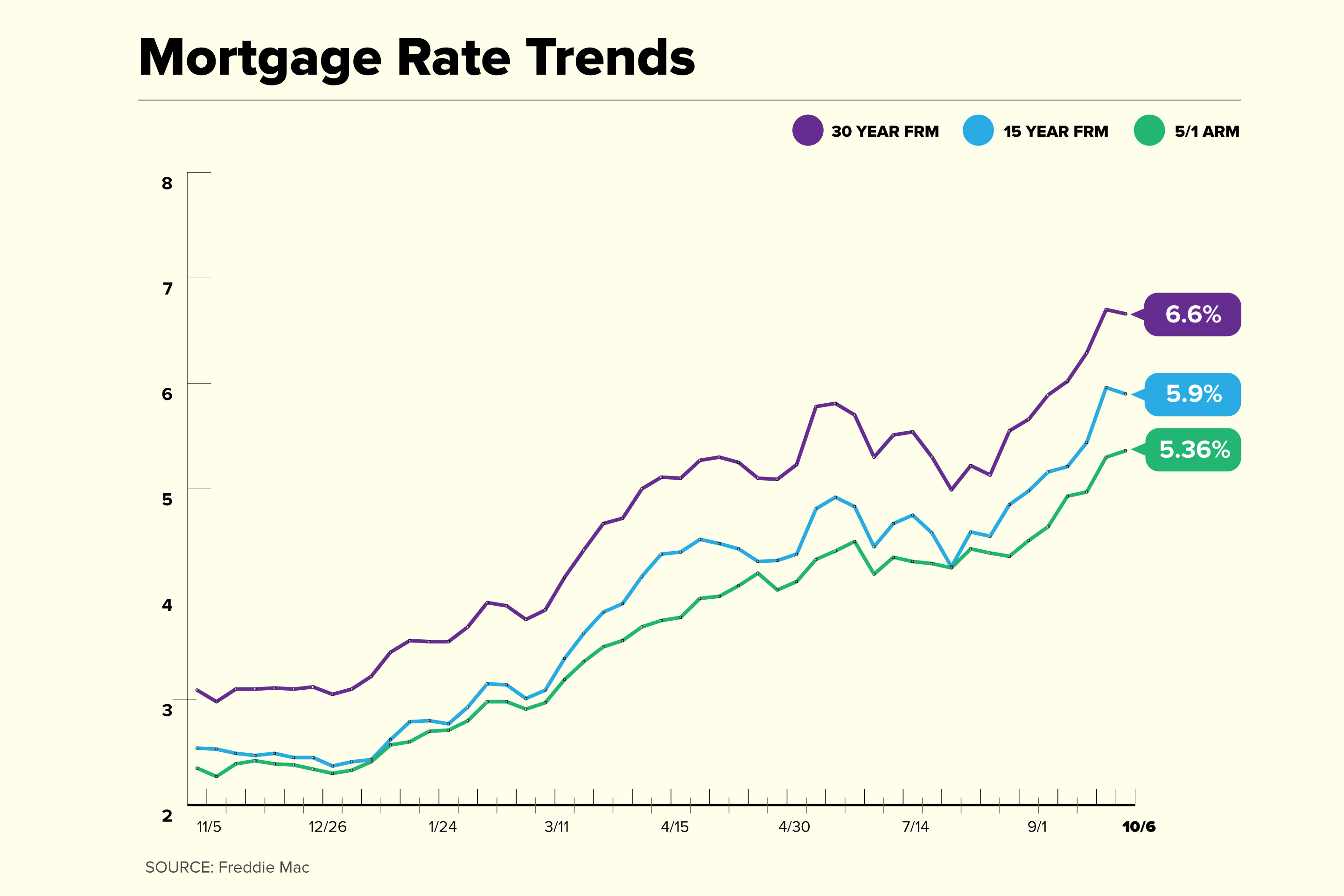

While mortgage rates are likely to rise over time, the rate you pay today could be lower than what you will pay in 2021 or ten. Lenders don't keep mortgages for very long. Fannie Mae/Freddie Mac then sells them the mortgages, which are packaged into mortgagebacked securities. These mortgages are then sold on to investors who buy them for more than government bonds.

Ratio loan-to value

When shopping for a mortgage, the loan-to-value ratio (LTV) is an important factor to consider. Your LTV should never exceed 80%. A higher LTV could mean higher borrowing costs and denial of the loan. To avoid problems later on, it is best to keep your loan amount below 80%.

An easy way to lower your LTV is by increasing the downpayment. With your lender, you can negotiate a lower price for the sale. The lower your loan-to-value ratio, the lower your interest rate will be.

FAQ

What should I do if I want to use a mortgage broker

A mortgage broker may be able to help you get a lower rate. Brokers are able to work with multiple lenders and help you negotiate the best rate. Some brokers do take a commission from lenders. Before you sign up for a broker, make sure to check all fees.

How much money do I need to save before buying a home?

It depends on the length of your stay. If you want to stay for at least five years, you must start saving now. But if you are planning to move after just two years, then you don't have to worry too much about it.

What can I do to fix my roof?

Roofs may leak from improper maintenance, age, and weather. Roofers can assist with minor repairs or replacements. Contact us to find out more.

What is reverse mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It works by allowing you to draw down funds from your home equity while still living there. There are two types: conventional and government-insured (FHA). Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers the repayment.

How many times can my mortgage be refinanced?

This will depend on whether you are refinancing through another lender or a mortgage broker. You can refinance in either of these cases once every five-year.

How can I get rid of termites & other pests?

Termites and other pests will eat away at your home over time. They can cause serious damage and destruction to wood structures, like furniture or decks. You can prevent this by hiring a professional pest control company that will inspect your home on a regular basis.

What flood insurance do I need?

Flood Insurance protects you from flooding damage. Flood insurance helps protect your belongings and your mortgage payments. Find out more about flood insurance.

Statistics

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How to become a real estate broker

You must first take an introductory course to become a licensed real estate agent.

The next thing you need to do is pass a qualifying exam that tests your knowledge of the subject matter. This involves studying for at least 2 hours per day over a period of 3 months.

After passing the exam, you can take the final one. You must score at least 80% in order to qualify as a real estate agent.

These exams are passed and you can now work as an agent in real estate.