It is important to take into account a variety of factors when choosing between an FHA loan and a USDA loan. In this article we will examine the credit score requirements and interest rates for each type. We also discuss geographic restrictions. This information will enable you to make an informed decision about the best loan for your needs.

Minimum credit score to get a USDA loan or a FHA loan

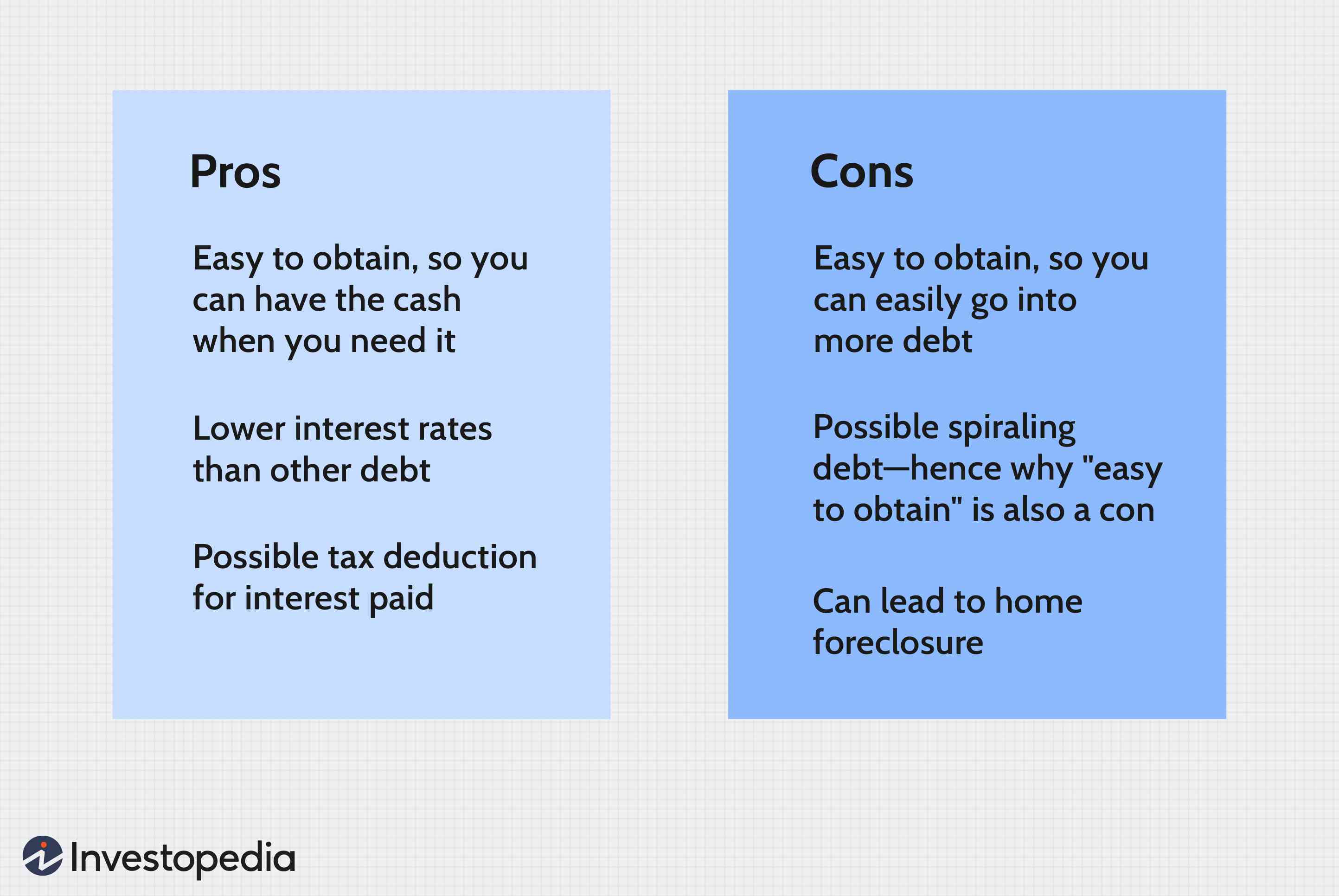

Consider your financial situation when comparing USDA loan minimum credit scores with FHA loans. Both programs allow individuals with poor credit to get loans. For example, you might qualify if your credit history includes a revolving account or divorce. You can still get a loan through a USDA loan. However, you will likely need to pay more down and make a smaller downpayment.

FHA loans have more flexibility and lower down payment requirements, but there are still limitations. USDA loans are only available in some areas. The FHA loan program, on the other hand, is available in all US counties.

For each type of loan, there are different interest rates

USDA loans are available to people with low credit scores. They can be qualified for a low interest rate. USDA loans can be obtained by those with as low credit scores as 580. These loans can also be used by those who are unable to afford a down payment for a conventional loan.

Both USDA and FHA loan programs have historically low interest rate. It is important to note that there are some differences between the two. While USDA loans may be more flexible, FHA loans may have stricter guidelines. Borrowers can't spend more than 31% on housing costs.

There is also a difference in the premium for mortgage insurance between the FHA and conventional loans. FHA loans require mortgage insurance, but this must be paid for the entire duration of the loan. USDA loans are exempt from mortgage insurance. FHA mortgage Insurance costs 0.85% of your loan amount. You must pay this monthly for the whole loan term. The loan term can last up to 11 years.

Geographic restrictions applicable to each type loan

The geographic restrictions for USDA and FHA loans may limit your ability to purchase a home. The USDA loan is available for single-family homes only in rural areas. It is not intended for those with less than 20,000 residents. FHA loans are for semi-rural and rural properties.

USDA loans are more flexible than FHA loans in terms of credit requirements. You may still be eligible for these loans even if you have poor credit. The USDA will require that your property be located in rural areas. But, it doesn't necessarily have to be farmland. In fact, almost 97% of the United States is considered rural. This means that even small communities and suburbs might be eligible to receive a USDA loan.

USDA loans are often called rural housing loans, but they are not limited to rural areas. USDA loan limits in some counties are lower than FHA loan limits. Los Angeles' FHA loan limit is higher than Montgomery's. A USDA loan limit for a single family home is lower than that for a whole city or county. Rural areas are a great option for first-time buyers.

FAQ

What is reverse mortgage?

Reverse mortgages allow you to borrow money without having to place any equity in your property. It works by allowing you to draw down funds from your home equity while still living there. There are two types of reverse mortgages: the government-insured FHA and the conventional. A conventional reverse mortgage requires that you repay the entire amount borrowed, plus an origination fee. If you choose FHA insurance, the repayment is covered by the federal government.

How can I calculate my interest rate

Market conditions can affect how interest rates change each day. The average interest rate for the past week was 4.39%. Divide the length of your loan by the interest rates to calculate your interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

What are the 3 most important considerations when buying a property?

The three most important things when buying any kind of home are size, price, or location. Location refers the area you desire to live. Price is the price you're willing pay for the property. Size refers to how much space you need.

What are the pros and cons of a fixed-rate loan?

Fixed-rate mortgages allow you to lock in the interest rate throughout the loan's term. This guarantees that your interest rate will not rise. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

How much money should I save before buying a house?

It depends on how much time you intend to stay there. It is important to start saving as soon as you can if you intend to stay there for more than five years. You don't have too much to worry about if you plan on moving in the next two years.

Statistics

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

External Links

How To

How to buy a mobile house

Mobile homes are houses that are built on wheels and tow behind one or more vehicles. Mobile homes are popular since World War II. They were originally used by soldiers who lost their homes during wartime. Mobile homes are still popular among those who wish to live in a rural area. These homes are available in many sizes and styles. Some houses are small while others can hold multiple families. Even some are small enough to be used for pets!

There are two types main mobile homes. The first is built in factories by workers who assemble them piece-by-piece. This takes place before the customer is delivered. You could also make your own mobile home. Decide the size and features you require. Next, ensure you have all necessary materials to build the house. To build your new home, you will need permits.

You should consider these three points when you are looking for a mobile residence. You may prefer a larger floor space as you won't always have access garage. A larger living space is a good option if you plan to move in to your home immediately. Third, make sure to inspect the trailer. Problems later could arise if any part of your frame is damaged.

You should determine how much money you are willing to spend before you buy a mobile home. It's important to compare prices among various manufacturers and models. Also, take a look at the condition and age of the trailers. Many dealerships offer financing options but remember that interest rates vary greatly depending on the lender.

You can also rent a mobile home instead of purchasing one. Renting allows for you to test drive the model without having to commit. However, renting isn't cheap. The average renter pays around $300 per monthly.