A home equity line is similar to a primary mortgage. Lenders will want to know how much equity you have in your home, how much the home appraised for, your income, outstanding debts, and your credit score before they can approve your loan. Lenders will need this information to validate their borrowers and ensure they are not high-risk credit borrowers. They also want to know the value of the collateral, which is your home.

How to get a home equity loan

A home equity loan can be used to finance major costs such as college tuition or home improvements. The Federal Reserve sets the interest rate. The Federal Funds rate is generally 3% lower than the prime rate. Tax deduction may be available for the interest rate on home equity line of credit.

A home equity loan allows borrowers to borrow cash based upon the home's worth, which is usually $50,000. The home equity line of credit works in the same way as a credit card but you only pay interest when you use it. Home equity lines offer discounts depending upon the amount of credit that you initially use.

To be eligible for a line of home equity credit, you must have a high credit score. While lenders generally accept credit scores between 700 and 700, there are some that will consider borrowers with lesser credit. However, it's important to keep your credit score as high as possible to get the best possible interest rate. Additionally, a home equity loan of credit allows you to access larger funds than personal loans or credit cards.

Repayment period

Consider a few things when determining the repayment time for a home-equity line of credit. First, ensure you have sufficient equity in your home to be eligible for the loan. Make sure you can afford the monthly increased payments. It is important to consider your debt-to–income ratio and credit score before making this final decision.

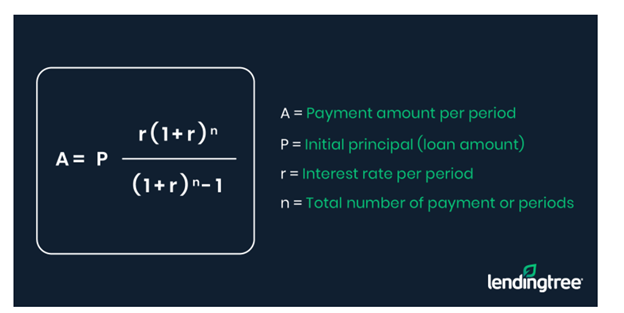

The repayment period for a home equity credit line is typically 5 to 10 year. You will pay monthly principal and interest payment during this period. This will help you pay off the debt faster and reduce your monthly payment. Depending on your situation, you may also want to consider using a payment plan to make your payments more affordable.

HELOCs can be used to loan money based on the property's value and the remaining balance on your mortgage. To ensure you are able to afford the loan, consult your financial advisor. A HELOC might not be right for you if your intention is to sell your house.

Interest rate

A home equity line is a type loan secured by a homeowner’s home. The rate of interest is variable and can depend on several factors such as your creditworthiness and the loan to value ratio. There are a few things you can do to make sure you get the best rate.

First, you must understand the operation of the loan. The typical home equity loan has two phases. One is the draw period, and one is the repayment period. The draw period is usually for around 10 years. During this time, you'll typically make small interest-only payments, with any additional payments going toward the principal.

A home equity line is a credit card that works similarly to a credit-card. However, you only pay interest for the amount you spend instead of the entire amount. The interest rates are usually lower than those of traditional mortgages and other types loans. HELOCs also have the advantage of not having to repay the whole amount immediately.

FAQ

What should I do before I purchase a house in my area?

It all depends on how many years you plan to remain there. It is important to start saving as soon as you can if you intend to stay there for more than five years. However, if you're planning on moving within two years, you don’t need to worry.

How can I fix my roof

Roofs can leak because of wear and tear, poor maintenance, or weather problems. Roofing contractors can help with minor repairs and replacements. Contact us for further information.

What are the three most important factors when buying a house?

The three most important things when buying any kind of home are size, price, or location. Location refers the area you desire to live. Price is the price you're willing pay for the property. Size is the amount of space you require.

What is reverse mortgage?

A reverse mortgage lets you borrow money directly from your home. It allows you access to your home equity and allow you to live there while drawing down money. There are two types: conventional and government-insured (FHA). Conventional reverse mortgages require you to repay the loan amount plus an origination charge. FHA insurance covers repayments.

Do I need flood insurance?

Flood Insurance covers flooding-related damages. Flood insurance can protect your belongings as well as your mortgage payments. Learn more about flood coverage here.

How can I calculate my interest rate

Market conditions impact the rates of interest. The average interest rate during the last week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. For example, if you finance $200,000 over 20 years at 5% per year, your interest rate is 0.05 x 20 1%, which equals ten basis points.

Statistics

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

External Links

How To

How to become an agent in real estate

An introductory course is the first step towards becoming a professional real estate agent. This will teach you everything you need to know about the industry.

The next step is to pass a qualifying examination that tests your knowledge. This requires you to study for at least two hours per day for a period of three months.

Once you have passed the initial exam, you will be ready for the final. To become a realty agent, you must score at minimum 80%.

Once you have passed these tests, you are qualified to become a real estate agent.