Foreclosure can have devastating effects on your credit score and ability to qualify for a mortgage. When faced with foreclosure, it is important that you take steps to recover your financial health and rebuild credit. Foreclosure can prevent you from buying a new home or qualifying for a new mortgage. To be able to purchase a home again, however, you must get your financial affairs in order.

Non-recourse mortgage states don't allow lenders to seize the personal assets of borrowers if the mortgage is not satisfied.

Non-recourse loans are more common in certain states. In these states, lenders cannot take a borrower’s personal assets if he or she defaults on a loan. The lender will only return the collateral property if the borrower defaults on a loan. The lender will not be able to seize personal assets unless the home is sold for less than the loan balance.

Higher interest rates

Your chances of getting a new loan, or even a job, can be affected if you have a foreclosure on credit. Many employers and landlords will review credit histories before hiring. Because lenders view you as high-risk, they will likely charge you more money to cover the risk. There are options to mitigate the negative effects of foreclosure and improve your credit score.

Waiting period

After a homeowner loses their house through foreclosure, the waiting time for repurchase can be quite long. However, there are certain requirements that can shorten this waiting period. Fannie Mae, Freddie Mac, and Fannie Mae have their own guidelines.

Neglected payments can have a negative impact on your credit score

Foreclosure, a major financial event, can have a wide range of effects on your credit scores. They depend on what credit reporting agency used and which credit scoring model was used. According to the Consumer Financial Protection Bureau, foreclosure stays on your report for seven years. However, the impact on your credit score is less severe if you are able to make your mortgage payments on time.

FHA loans

If you want to purchase a home after foreclosure, you should consider applying for FHA loans. FHA loans are a great option for those with lower credit scores and low down payments. Foreclosures can often be priced lower than comparable homes on the market. When you combine the low price with an FHA loan, you can save thousands of dollars on your home and still own it.

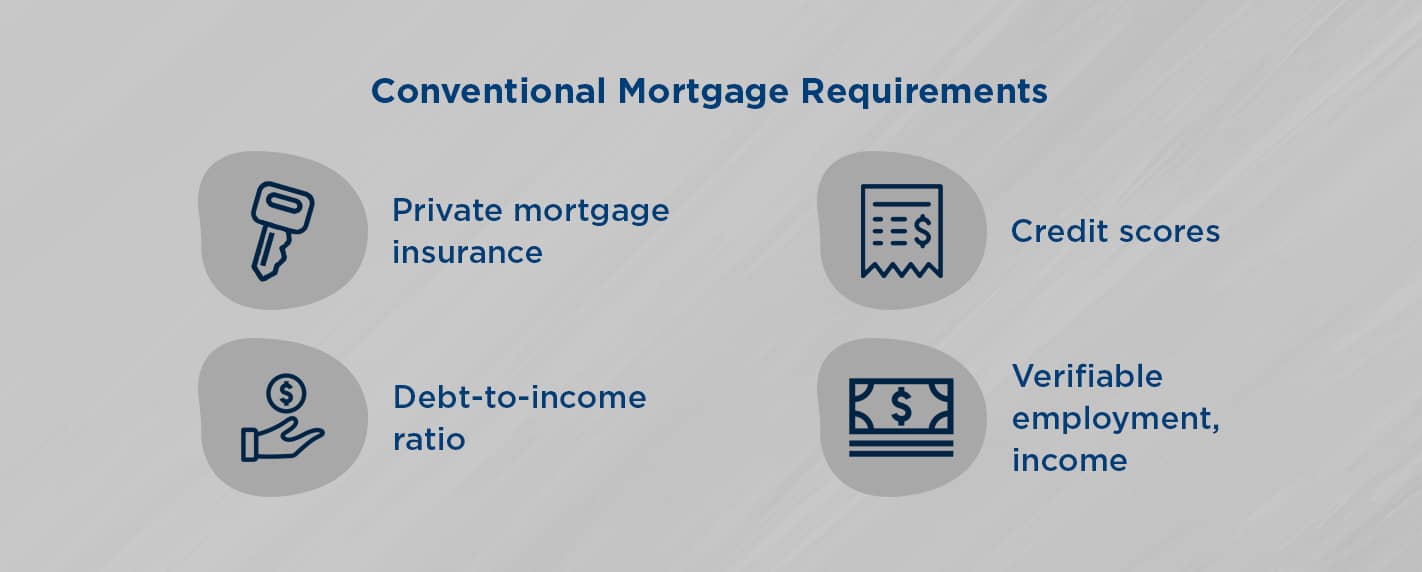

Conventional loans

Even though a foreclosure could make it difficult to obtain a conventional loan for your home, there are still ways to increase your chances. It is important to choose the right lender. Each lender has slightly different approval requirements.

FAQ

How can I get rid Termites & Other Pests?

Termites and many other pests can cause serious damage to your home. They can cause serious destruction to wooden structures like decks and furniture. It is important to have your home inspected by a professional pest control firm to prevent this.

How can you tell if your house is worth selling?

If your asking price is too low, it may be because you aren't pricing your home correctly. Your asking price should be well below the market value to ensure that there is enough interest in your property. You can use our free Home Value Report to learn more about the current market conditions.

What is the average time it takes to sell my house?

It depends on many factors including the condition and number of homes similar to yours that are currently for sale, the overall demand in your local area for homes, the housing market conditions, the local housing market, and others. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

How many times may I refinance my home mortgage?

It all depends on whether your mortgage broker or another lender is involved in the refinance. You can refinance in either of these cases once every five-year.

Statistics

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

External Links

How To

How do you find an apartment?

Moving to a new place is only the beginning. This takes planning and research. It involves research and planning, as well as researching neighborhoods and reading reviews. You have many options. Some are more difficult than others. Before renting an apartment, it is important to consider the following.

-

Researching neighborhoods involves gathering data online and offline. Online resources include Yelp and Zillow as well as Trulia and Realtor.com. Local newspapers, real estate agents and landlords are all offline sources.

-

See reviews about the place you are interested in moving to. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also check out the local library and read articles in local newspapers.

-

For more information, make phone calls and speak with people who have lived in the area. Ask them about their experiences with the area. Ask if they have any suggestions for great places to live.

-

You should consider the rent costs in the area you are interested. You might consider renting somewhere more affordable if you anticipate spending most of your money on food. You might also consider moving to a more luxurious location if entertainment is your main focus.

-

Find out information about the apartment block you would like to move into. What size is it? What is the cost of it? Is it pet friendly What amenities does it have? Are there parking restrictions? Are there any rules for tenants?