A second mortgage is a great option if you are insolvent or have a high-interest mortgage. It can also help you build equity in a home. There are also some drawbacks. Before deciding if a second mortgage is right to you, it's important that you consider all these factors.

Home equity loan

You must consider your financial situation before you apply for a home equity loan to help you pay off your second mortgage. Most lenders require a minimum credit score of 620, but some require a score of as high as 680. Pay down all your debts and correct any errors in your credit report to improve your credit score. Get at least three quotes form different lenders. This will help you compare rates.

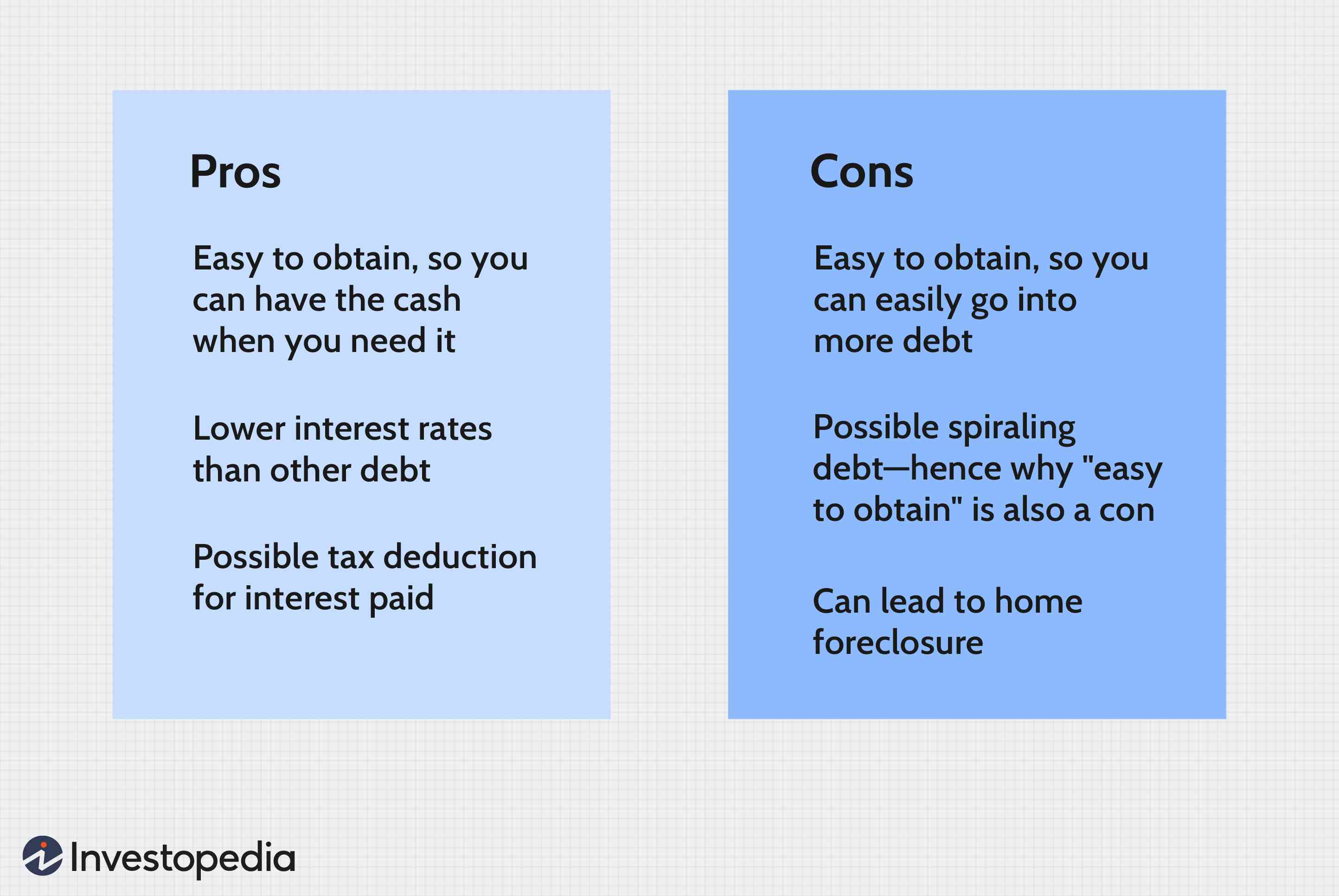

A home equity loan, also known by the second mortgage, is an unsecure loan that uses your house as collateral. Your home can be used as collateral for up to 80 percent. Lenders have the right to foreclose on your property and claim it as a loss in the event that you default on your loan.

If you require extra cash for an expensive purchase, home equity loans can be a great option. These loans typically have low monthly payments and an interest rate that is fixed. Another benefit of home equity loans are the fact that they can be paid off over a specific period of money. Because you can make monthly installments until you reach a zero balance, these loans are ideal for debt consolidation.

A home equity loan may not be the best choice for everyone, but they may be a good option if you need money for an unforeseen expense. The interest you pay could be tax-deductible and your monthly payments might be lower than your monthly mortgage payment.

Credit for home equity

A home equity line of credit is an excellent way to borrow money against your home's equity. This is money you can access when your home needs additional funds, such as for urgent repairs or large-scale remodels. It's best to not treat this credit like a credit card, even though the interest you pay is tax-deductible. Instead, you should use this money to invest in productive ways.

One way to avoid falling into this trap is to only borrow the amount you need, and then pay it back. Home equity loans are a great way for you to convert your equity into cash if you're able to make your payments on-time. The extra money can go towards home renovations, or other improvements that will improve the value of your house. You should not take out home equity loans if your financial situation isn't clear.

You must meet a few requirements to be eligible for a home-equity line of credit. To be eligible for a home equity line of credit, you must first have at least 15% equity. A second requirement is that your debt-to-income ratio is less than 40%. To qualify, you will need equity of at least $40,000

FAQ

How long will it take to sell my house

It depends on many different factors, including the condition of your home, the number of similar homes currently listed for sale, the overall demand for homes in your area, the local housing market conditions, etc. It can take from 7 days up to 90 days depending on these variables.

How many times do I have to refinance my loan?

This depends on whether you are refinancing with another lender or using a mortgage broker. In both cases, you can usually refinance every five years.

Are flood insurance necessary?

Flood Insurance protects you from flooding damage. Flood insurance protects your possessions and your mortgage payments. Find out more information on flood insurance.

How much does it cost for windows to be replaced?

Windows replacement can be as expensive as $1,500-$3,000 each. The total cost of replacing all your windows is dependent on the type, size, and brand of windows that you choose.

How do you calculate your interest rate?

Market conditions influence the market and interest rates can change daily. The average interest rate for the past week was 4.39%. To calculate your interest rate, multiply the number of years you will be financing by the interest rate. Example: You finance $200,000 in 20 years, at 5% per month, and your interest rate is 0.05 x 20.1%. This equals ten bases points.

Can I buy my house without a down payment

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include government-backed mortgages (FHA), VA loans and USDA loans. More information is available on our website.

What are the key factors to consider when you invest in real estate?

First, ensure that you have enough cash to invest in real property. You will need to borrow money from a bank if you don’t have enough cash. It is also important to ensure that you do not get into debt. You may find yourself in defaulting on your loan.

You also need to make sure that you know how much you can spend on an investment property each month. This amount should cover all costs associated with the property, such as mortgage payments and insurance.

Finally, you must ensure that the area where you want to buy an investment property is safe. It would be best if you lived elsewhere while looking at properties.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

Moving to a new place is only the beginning. This requires planning and research. It involves research and planning, as well as researching neighborhoods and reading reviews. This can be done in many ways, but some are more straightforward than others. These are the steps to follow before you rent an apartment.

-

You can gather data offline as well as online to research your neighborhood. Online resources include Yelp. Zillow. Trulia. Realtor.com. Local newspapers, landlords or friends of neighbors are some other offline sources.

-

Find out what other people think about the area. Yelp and TripAdvisor review houses. Amazon and Amazon also have detailed reviews. Local newspaper articles can be found in the library.

-

Call the local residents to find out more about the area. Talk to those who have lived there. Ask them what the best and worst things about the area. Ask them if they have any recommendations on good places to live.

-

You should consider the rent costs in the area you are interested. Consider renting somewhere that is less expensive if food is your main concern. Consider moving to a higher-end location if you expect to spend a lot money on entertainment.

-

Learn more about the apartment community you are interested in. It's size, for example. What's the price? Is the facility pet-friendly? What amenities does it have? Are you able to park in the vicinity? Do tenants have to follow any rules?