Home equity loans are secured installment loans you can take out against the home's value. They have a fixed rate of interest and fees and are less flexible than home equity lines of credit. If you're thinking of applying for a home equity loan, there are a few important steps you should take first.

Fixed-rate home equity loan are loans that you can get secured by your home's worth.

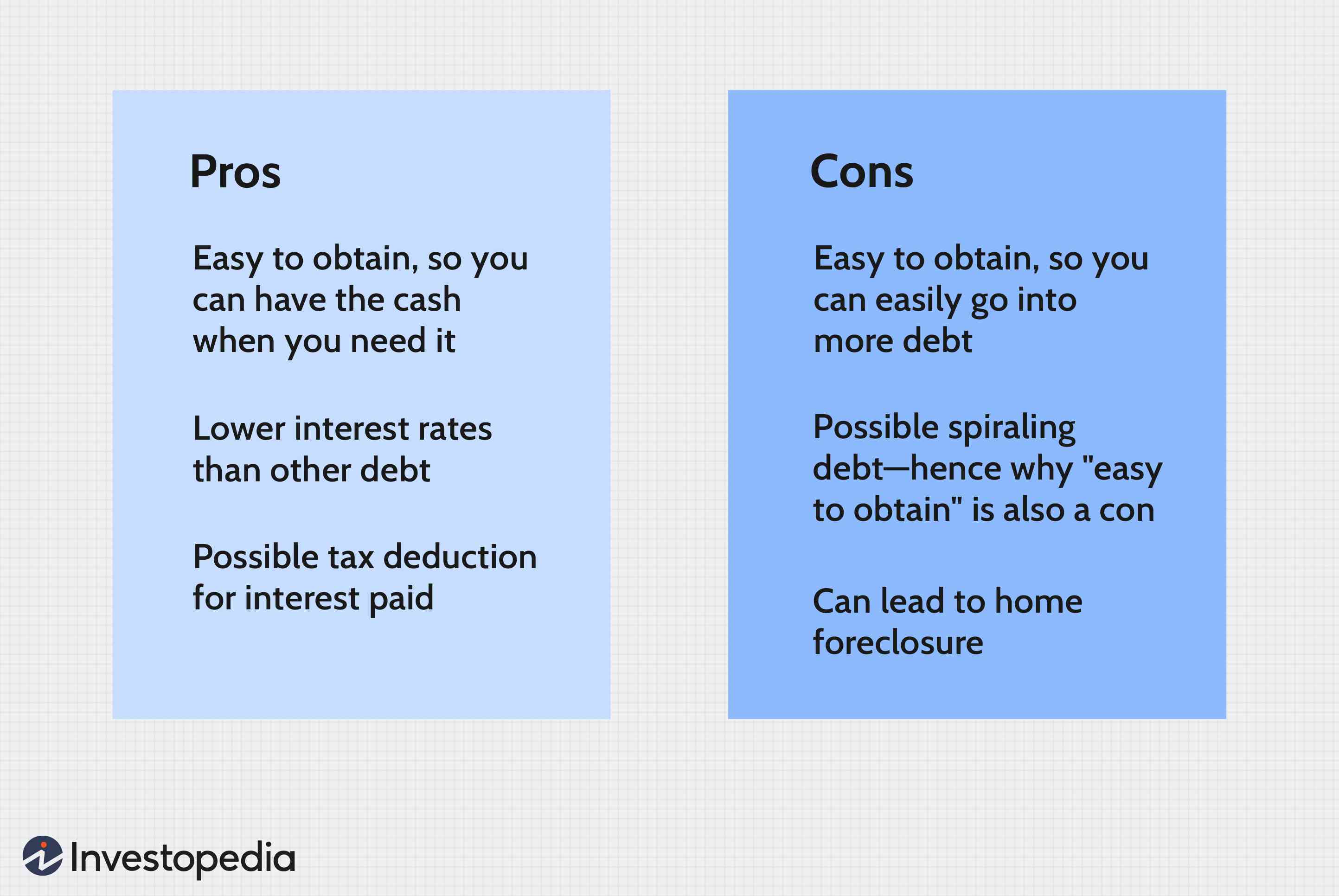

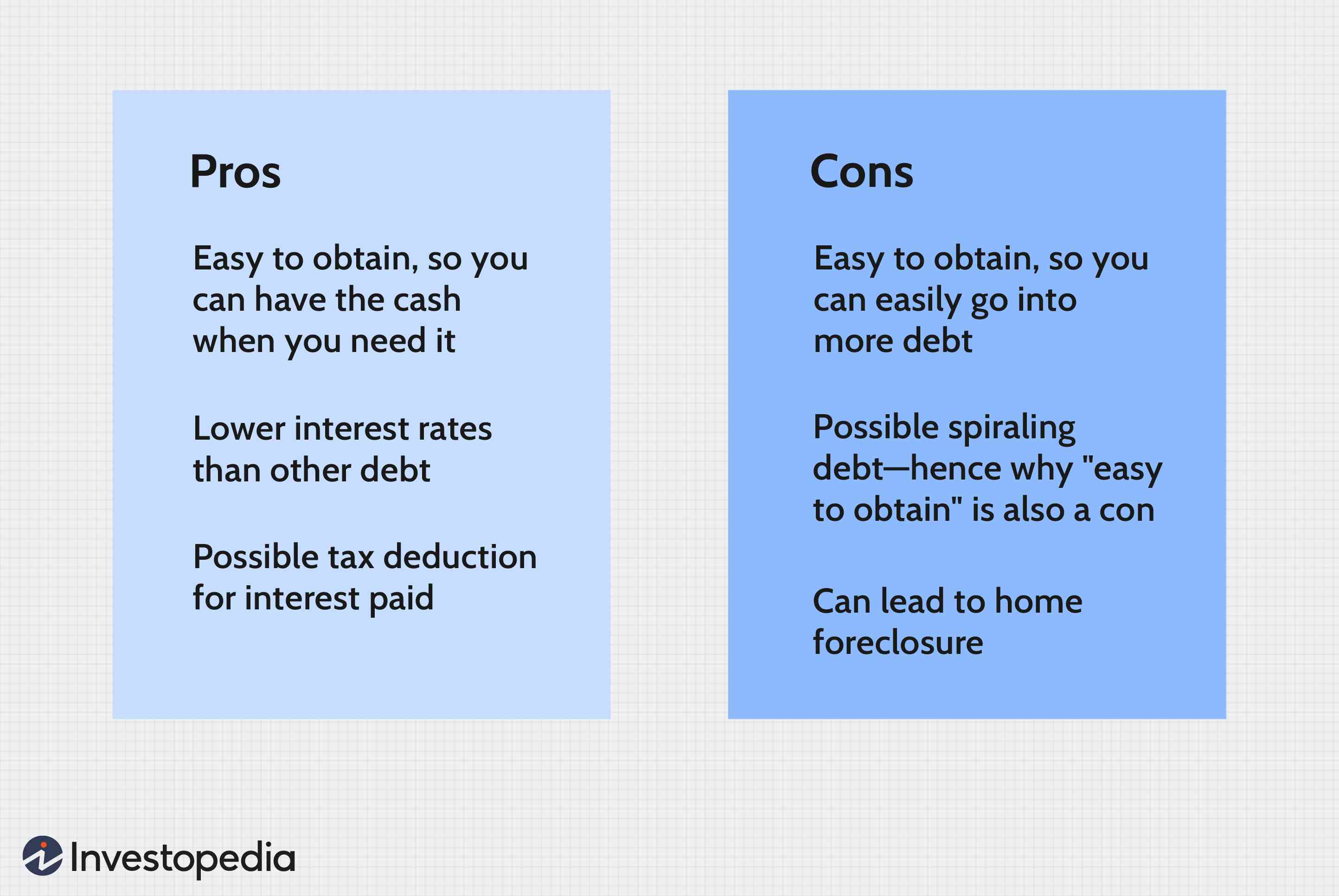

A home equity loans is a loan that's secured by your home. These loans are predictable because they have fixed interest rates and long loan terms. These loans can be a great option for those who need to consolidate debt and are facing large monthly expenses. Not only are they predictable, but you may also be eligible for tax deductions with home equity loans.

A home equity loan is often more affordable than a HELOC. The interest rate is fixed, unlike an HELOC, which can increase or decrease depending on national benchmarks. While these loans are great for emergency purchases, they're not a great option for large loans. A home equity loan is a fixed-interest loan that can help you manage your finances more effectively.

They have a variable-interest rate

Variable interest rates are a key consideration when applying for home equity loans. Even if your credit score falls below 620, you might still be eligible for one of these loans. However you will pay more interest rates and fees. You may not be able to repay your loan if you have a low credit rating. This has led to more strict lending practices and increased restrictions on this type of loan.

Variable rate home equity loans come in many forms including HELOCs which function like a credit card. HELOC interest rates change with the prime rate. Your payments will be affected by the interest rate and the time required to repay the loan. HELOCs can have a draw term of up to 10 year. HELOCs can offer low interest rates at the beginning.

They have higher fees

In many ways, home equity loans differ from personal loans. First, they are more accessible than personal loans. Second, they are less risky to lenders. A home equity loan is secured by the homeowner, giving the lender greater protection if the borrower defaults. Home equity loans often have lower interest rates.

Home equity loan fees can also vary by lender. Some charge an origination cost when you apply for a loan. Other lenders add it to your loan total. These fees can range from $0 up to $125. Some lenders may also charge an application fees to complete the loan application. A credit report fee is another fee that home equity loans may incur. It usually costs around $25.

They are more flexible than a home-equity line of credit, but they are still available.

Home equity lines of credit work much like credit cards. They allow you to get the money you need as soon as it is available. You can draw on the money at any time during the draw. Some lenders will even allow interest-only payments. This can make your payments higher, but it can help you pay off the credit when you're done using it.

Another downside to a home equity loan is the impact it will have on your credit score. A home equity loan will have a greater impact than a line of credit, but it all depends on how much your home owes and the interest rate. Lenders require that borrowers have a minimum credit score of 620. However, some lenders will allow borrowers with lower credit scores to apply for home equity loan. The higher your credit score, the better the interest rates and loan terms will be.

They can help with consolidating debt

A home equity mortgage may be a good option if you want to consolidate debt. A home equity loan can help you lower your interest rate and reduce your monthly payments. This type is more affordable than most other types of loans. The interest you pay could even be tax-deductible. It's a great option for those with high interest credit card balances, or for people who want to streamline their expenses. However, there are risks associated with this type of loan. The loan may not be repayable and you could lose your home if you default on payments.

A debt consolidation loan consolidates multiple debts into a single loan with one interest rate and one monthly repayment. This type loan can be obtained from many lenders, including banks or credit unions. Online applications can also be made to lenders for debt consolidation loans. Some of these sites offer same-day approval, making the process even faster.

FAQ

Is it possible for a house to be sold quickly?

If you have plans to move quickly, it might be possible for your house to be sold quickly. But there are some important things you need to know before selling your house. First, find a buyer for your house and then negotiate a contract. Second, prepare the house for sale. Third, it is important to market your property. You must also accept any offers that are made to you.

What is the average time it takes to sell my house?

It all depends on several factors such as the condition of your house, the number and availability of comparable homes for sale in your area, the demand for your type of home, local housing market conditions, and so forth. It takes anywhere from 7 days to 90 days or longer, depending on these factors.

How many times may I refinance my home mortgage?

It depends on whether you're refinancing with another lender, or using a broker to help you find a mortgage. In both cases, you can usually refinance every five years.

Is it cheaper to rent than to buy?

Renting is usually cheaper than buying a house. It is important to realize that renting is generally cheaper than buying a home. You will still need to pay utilities, repairs, and maintenance. The benefits of buying a house are not only obvious but also numerous. You will be able to have greater control over your life.

Statistics

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- The FHA sets its desirable debt-to-income ratio at 43%. (fortunebuilders.com)

- It's possible to get approved for an FHA loan with a credit score as low as 580 and a down payment of 3.5% or a credit score as low as 500 and a 10% down payment.5 Specialty mortgage loans are loans that don't fit into the conventional or FHA loan categories. (investopedia.com)

- Some experts hypothesize that rates will hit five percent by the second half of 2018, but there has been no official confirmation one way or the other. (fortunebuilders.com)

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

External Links

How To

How to Find Houses to Rent

Renting houses is one of the most popular tasks for anyone who wants to move. However, finding the right house may take some time. When it comes to choosing a property, there are many factors you should consider. These include location, size, number of rooms, amenities, price range, etc.

To make sure you get the best possible deal, we recommend that you start looking for properties early. Ask your family and friends for recommendations. This will give you a lot of options.