A type of mortgage called the 80-10-10 loan allows borrowers with less than 20% down payment to get rid of PMI. They are also able to purchase a very expensive home without needing to obtain a large loan. The downside to this type of loan is that you will need to get two mortgages at once.

Piggyback loan

Piggyback loans allow you to make a smaller down payment on your new house than other types of mortgages. The 80-10-10 Loan requires only 10% downpayment, unlike other types. However, you may have to pay mortgage insurance on the loan as well. If you are able to repay the loan on time and have good credit, this mortgage loan may be a good option.

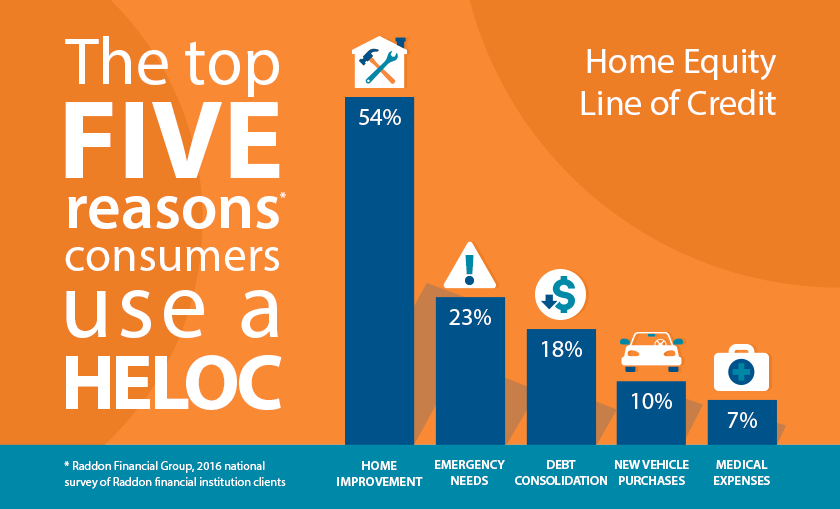

A piggyback loan is made up of two types of lien: the first is a fixed rate mortgage that covers as much as 80% of the home's price. The second lien, however, is a home Equity Line of Credit (HELOC). Although they are similar in structure to credit cards credit cards, home equity lines can of credit (HELOCs), have no interest rates and can be repaid at any time.

Jumbo loans

With 80-10-10 loans, borrowers can buy larger homes with a smaller downpayment. This allows them to avoid the strict guidelines that are involved with jumbo loans. They don't have to pay 20% of the home's total price. Instead, they can pay 10% which will significantly reduce their monthly payments. These loans are perfect for people who are in financial distress or those who can't afford the down payment on a conventional loan.

The loan limit for jumbo mortgages varies from lender to lender but is usually greater than $647,000. The limit for Hawaii or Alaska is $970,800.

80 10 10 loans

A 80/10/10 loan is a great option for those who are interested in a costly home, but have limited funds. These loans allow you to borrow 80% of the purchase price, but require a small down payment of 10%. Additionally, these loans do not require mortgage insurance.

These loans are an attractive option for homeowners looking to avoid jumbo debt, reduce PMI, or buy a house after selling their old one. These loans are similar to piggyback loans. Although there are many variations of this loan, the principle is the same. You take out two loans: one for your new home, and one for your existing home. The second loan is then paid off with the first. The upside to this type of loan is that you can buy a higher-priced home and avoid paying PMI.

Rural housing loans

Rural housing loans are a great way to purchase a new home. These loans are guaranteed by the USDA and are great for those with low income. This government program offers low rates of interest and 0% down payment. It provides guidance to homebuyers on the application process, eligibility requirements, and how to apply. It offers refinancing of qualified loans.

Rural housing loans can be used for a variety of purposes. They can be used by buyers to buy their first or a second home. An FHA mortgage is only 3.5% of the purchase price. This allows individuals with low incomes and lower incomes to afford a mortgage with lower monthly payments.

USDA loans

A USDA 80-10-10 loan may be the right loan for you if you need a no-down mortgage. This program is especially designed for low- to moderate-income households. To be eligible, you must meet certain income requirements and property requirements. These are the requirements that you must meet to be able buy a house.

There are many options for this loan program. These include self-serviced loans as well as bank-owned loans. These loans are guaranteed to offer low-interest rates and flexible payments. You can repay these loans in as little as 33 to 38 year depending on your income.

FAQ

What are the benefits to a fixed-rate mortgage

A fixed-rate mortgage locks in your interest rate for the term of the loan. You won't need to worry about rising interest rates. Fixed-rate loan payments have lower interest rates because they are fixed for a certain term.

Is it possible sell a house quickly?

If you have plans to move quickly, it might be possible for your house to be sold quickly. You should be aware of some things before you make this move. First, you must find a buyer and make a contract. Second, prepare your property for sale. Third, you must advertise your property. You should also be open to accepting offers.

How do you calculate your interest rate?

Market conditions influence the market and interest rates can change daily. The average interest rates for the last week were 4.39%. Divide the length of your loan by the interest rates to calculate your interest rate. For example: If you finance $200,000 over 20 year at 5% per annum, your interest rates are 0.05 x 20% 1% which equals ten base points.

Is it possible to get a second mortgage?

Yes. However, it's best to speak with a professional before you decide whether to apply for one. A second mortgage is typically used to consolidate existing debts or to fund home improvements.

Can I buy a house in my own money?

Yes! There are many programs that can help people who don’t have a lot of money to purchase a property. These programs include conventional mortgages, VA loans, USDA loans and government-backed loans (FHA), VA loan, USDA loans, as well as conventional loans. Visit our website for more information.

How much does it cost to replace windows?

Windows replacement can be as expensive as $1,500-$3,000 each. The exact size, style, brand, and cost of all windows replacement will vary depending on what you choose.

What should I be looking for in a mortgage agent?

A mortgage broker is someone who helps people who are not eligible for traditional loans. They shop around for the best deal and compare rates from various lenders. Some brokers charge a fee for this service. Some brokers offer services for free.

Statistics

- This means that all of your housing-related expenses each month do not exceed 43% of your monthly income. (fortunebuilders.com)

- 10 years ago, homeownership was nearly 70%. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

External Links

How To

How to Find an Apartment

When moving to a new area, the first step is finding an apartment. This process requires research and planning. This involves researching and planning for the best neighborhood. This can be done in many ways, but some are more straightforward than others. Before renting an apartment, you should consider the following steps.

-

Online and offline data are both required for researching neighborhoods. Online resources include websites such as Yelp, Zillow, Trulia, Realtor.com, etc. Other sources of information include local newspapers, landlords, agents in real estate, friends, neighbors and social media.

-

Review the area where you would like to live. Review sites like Yelp, TripAdvisor, and Amazon have detailed reviews of apartments and houses. You can also find local newspapers and visit your local library.

-

Make phone calls to get additional information about the area and talk to people who have lived there. Ask them what they liked and didn't like about the place. Ask for recommendations of good places to stay.

-

Be aware of the rent rates in the areas where you are most interested. Renting somewhere less expensive is a good option if you expect to spend most of your money eating out. If you are looking to spend a lot on entertainment, then consider moving to a more expensive area.

-

Find out all you need to know about the apartment complex where you want to live. How big is the apartment complex? What is the cost of it? Is it pet friendly What amenities does it offer? Are you able to park in the vicinity? Do tenants have to follow any rules?